10 income tax rules that are effective from April 2022

Vaishali resumed work in 2021 after taking a sabbatical for three years. Although she had investments and had to pay taxes on her passive income, she had to inform her accountant, Mohit, about her job and other investments she made this year. He sent her the tax to be paid along with the calculations. Soon after seeing the mail, she called Mohit to discuss it in detail.

Tax Rule #1 - Dividends from Assets of All Classes Taxable

The conversation started with a concerned Vaishali asking about the new tax rule on dividends earned from mutual funds. She received a good amount of income as dividend from her portfolios. Mohit explained that the dividends she earned last year would be taxed as per her tax slab and that this rule has been in effect since April 2020 for the sale of mutual funds and listed stocks. However, from this year onwards, the existing 15% surcharge on Long term capital gains through sale would extend to other asset classes including physical gold, real estate properties, debentures, debt funds, and others.

When Vaishali asked if there was a way to improve her tax slab, Mohit recommended she switch to a growth option in her mutual funds. This way, her portfolio value increases without additional tax implications. He also explained now that she is earning from her regular job, she can afford to do the switch without any direct impact on her lifestyle.

Tax Rule #2 - Tax on Digital Assets

Next, Vaishali moved the conversation to cryptocurrencies. She expressed that while the crypto regulations were still developing at the beginning of 2021, there was a lot of promise in the space. She had made a bold choice of trading in various cryptocurrencies and, more recently, in NFTs. However, the trade had not yielded the results she had hoped for.

Vaishali wanted to clarify if the profit/loss set-off would be the same as other fund classes. Mohit shared that a 30% tax would be levied on her profits from the sale of cryptocurrency. He also explained how the profits could not set off the loss she made from selling off another crypto asset.

Tax Rule #3 - TDS on Digital Assets as Gifts

Additionally, he also shared how 1% TDS will be levied on every crypto transaction, whether it is a purchase or sale of an asset, including those received as gifts.

Tax Rule #4 - Timeframe Increased to Revise Previous Tax Returns

Before Vaishali could ask another question, Mohit underlined one of the most beneficial rules that were implemented this year: the window to revise tax returns has increased from 5 months to 2 years from the due date of filing the return. Vaishali had previously mentioned to Mohit about missing the window to revise her FY 2021-22 return, and this rule will help her remedy that situation.

Tax Rule #5 - Deduction Claim on NPS Contribution

Vaishali’s father was a state government employee who also contributed to the National Pension Scheme (NPS). She asked him about her father’s tax status. Mohit explained that investing in the NPS is a good choice for a person of her father’s age as it promises a flow of money after the age of 60. Mohit could see a visibly elated Vaishali when she learned that state government employees could now claim up to 14% deduction under Section 80CCD(2) for NPS contribution.

Tax Rule #6 - Limit on Provident Fund Contribution

He also informed her to keep her father’s contribution towards Provident Fund under INR 2.5 lakhs as the new rule implemented a tax on amounts beyond the said limit.

Tax Rule #7 - New Revision to Rule 80EEA

Vaishali seemed to have gained better clarity on her financials when a question popped into her head about home loans. She had recently purchased an apartment by taking out a loan and hoped to get a tax exemption on the interest paid. Mohit informed her that the previous deduction of up to INR 1.5 lakh on home loan interest for house property valued less than INR 45 lakhs under Section 80EEA is no longer available, but other home loan interest deductions up to INR 2 lakhs will remain valid as Section 24 of the Income Tax Act.

Moreover, as far as Vaishali was concerned, she had received her home loan sanction letter before 1st April 2022, making her eligible for the claim for the entire tenure of the home loan.

There were a few more clarifications pending, and Mohit was quick. Although Mohit had explained everything in detail, he knew Vaishali might need some notes to understand the new updates that came into existence this year. He showed her a table with three new additional rules and sent it to her via email for future reference:

Tax Rule #8 - Tax Claim on Insurance

The parent/guardian of a person with a disability can claim a tax deduction on health insurance taken on behalf of the concerned person

Tax Rule #9 - Tax Exemption for COVID-19 Medical Expenses

Tax exemptions shall be provided to those who received money for COVID-19 medical treatment

Tax Rule #10 - COVID-19 Tax Exemption on Compensation Received by Family

Up to INR 10 lakhs of relief received by a family member of a COVID-19 deceased patient will be tax exempted

As they reached the end of the discussion, Mohit asked Vaishali to choose between the new and old tax regime. He suggested that while the new budget rules and their impact on Vaishali’s financials were being discussed, she must also take time to understand the rules that have come into play in 2020. While the new regime offered more slabs with lower tax rates, Mohit recommended that she take a decision on the basis of investment requirements and current financial commitments. He also shared a detailed blog, highlighting the difference between the old and new tax regimes for a holistic understanding.

Old vs. New Tax Regime: A brief overview

| Old Tax Rules | New Tax Rules |

| Long term capital gains (LTCG) earned from sale/transfer of equities and equity mutual funds are levied a maximum surcharge of 15%. | Long term capital gains made from sale/transfer of all types of assets including physical gold, real estate properties, debentures, debt funds will incur a surcharge of 15% |

| All contributions towards PF were tax-free | Any contribution above INR 2.5 lakhs towards PF will be taxable |

| Revisions in the tax return can be made within five months from the due date of filing return | Revisions in the tax return can be made within 2 years from the due date of filing return |

| Deduction of up to INR 1.5 lakh on home loan interest for a house property less than INR 45 lakhs will be exempted under Section 80EEA | Deduction of up to INR 1.5 lakh on home loan interest under Section 80EEA is no longer available |

| Central government employees are allowed to claim tax benefit of 14% for the employer's contribution to their NPS accounts. | State government employees also are allowed to claim a tax benefit of 14% for the employer's contribution to their NPS accounts. |

Mohit also included a table on income tax slabs, for Vaishali’s quick reference:

| Total income | New tax regime | Old tax regime |

| Upto INR 2.5 lakhs | Nil | Nil |

| INR 2.5 lakhs to INR 5 lakhs | 5% | 5% |

| INR 5,00,001 to INR 7.5 lakhs | 10% | |

| INR 7,50,001 to INR 10 lakhs | 15% | 20% |

| INR 10,00,001 to INR 12.5 lakhs | 20% | |

| INR 12,50,001 to INR 15 lakhs | 25% | 30% |

| INR 15,00,001 and above | 30% |

Vaishali was grateful to receive this summary and knew her weekend will be spent reading and understanding RBL Bank’s blog on the two tax regimes in order to plan her investments better for the current financial year.

While tax planning is a long and tedious process, it is imperative to remain informed of the new changes and updates. This will help make modifications to the investment strategy and avoid any last-minute surprises.

Disclaimer: RBL Bank Limited is merely displaying services/ offers provided by third party(ies) and RBL Bank is not rendering any of these services/offers. RBL Bank is neither endorsing third party(ies)/services nor responsible for the quality of the services offered/products by third party(ies). RBL Bank will not bear any obligation or liability if a customer avails such services of third party(ies). All service-related queries/complaints will be addressed to the respective third party(ies) only. The customer is free to avail of such services from any other sources/platforms.

Disclaimer: Articles published on the website are merely indicative and suggestive in nature and do not amount to solicitation. The contents do not guarantee the desired returns and/or results. Reader is advised to exercise discretion and consult independent advisors for achieving desired result. Visitors to this blog/ website w.r.t products & services offered by RBL Bank Limited herein, shall ensure that the comments / feedback posted shall be restricted to the contents published herein and shall not contain such language that may be un-parliamentary or against any religion, caste, section of society, political view etc. While our endeavor is to publish the comments that are submitted, however, all comments/feedback shall be subject to internal review by RBL Bank Limited. We do not guarantee that the comments that are submitted will be published.

The Rise of Digital Arrest: Safeguard Your Data from Cybercriminals

In this blog, we will explore "Digital Arrest," its risks, and practical tips to safeguard your online security.

Nov 21, 2024

Nov 21, 2024

How to Protect Yourself from Social Engineering Attacks

This blog covers how social engineering attacks work and offers essential tips to recognise and prevent them.

Nov 04, 2024

Shop Safely Online: Key Tips for Secure Online Shopping

This blog covers five essential tips for safe online shopping, including secure websites, safe payments, and protecting personal information.

Oct 31, 2024

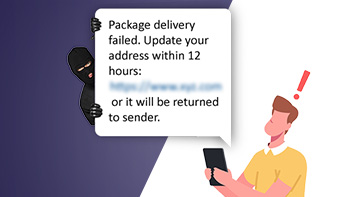

How the India Post Delivery Scam Works and How to Avoid It

In this blog, we will uncover how the India Post delivery scam works, highlight warning signs, and share tips to help you stay secure.

Oct 29, 2024

Comprehensive Guide to Zero Balance Savings Accounts in India

In this blog, we will explore Zero Balance Savings Accounts, their benefits, features, and eligibility.

Oct 25, 2024

Credit Cards: A Guide to Maximising Your Card's Potential

Unlock the full potential of credit cards with this comprehensive guide on benefits, types, and application tips.

Oct 18, 2024

Shop Smart, Save Big: How to Maximise Credit Card Benefits

In this blog, we will explore how to maximize your credit card benefits and unlock savings this festive season.

Oct 10, 2024

Investment Fraud: How to Safeguard Your Finances

Learn how to recognize and protect yourself from investment fraud. Discover key strategies to safeguard your money and avoid common scams.

Oct 01, 2024

6 Tips for Effective Savings Account Management

Learn key tips to manage your savings: maximize interest, maintain MAB/QAB, monitor fees, and leverage digital banking for better financial health.

Sep 21, 2024

Know the eligibility criteria applicable for a Credit Card

This blog covers key eligibility criteria and required documents for obtaining a credit card, guiding you through the application process.

Sep 13, 2024

How to Spot and Avoid Impersonation Scams

This blog explores how impersonation scams work, highlights warning signs, and offers tips to protect yourself from these sophisticated frauds.

Sep 02, 2024

Shop Smarter, Save Better: Discover ShopRite Credit Card

Turn everyday shopping into rewards with the RBL Bank ShopRite Credit Card. Earn cashback, rewards points, and exclusive benefits. Read more...

Aug 23, 2024

Understanding Benefits of Fixed Deposits for Senior Citizens

This blog highlights the key benefits of fixed deposits (FDs) for senior citizens and why they remain a secure, reliable investment choice.

Aug 14, 2024

How Can You Avoid Falling into the Fraudster’s Trap

This blog covers how to protect your personal and financial information from digital fraud by identifying common scams and following key safety practices.…

Aug 05, 2024

Why should women have their own Savings Account?

In this blog, we explore the significance of women having personal savings accounts, promoting financial independence, literacy, and empowerment.

Jul 29, 2024

Credit Card EMI: Empowering Your Purchasing Power

In this blog, we explore how EMI on Credit Cards lets you convert large purchases into manageable payments, offering flexibility and budgeting.

Jul 15, 2024

How to Protect Your Device from APK Fraud?

In this blog, we will explore APK fraud, where cybercriminals trick users into installing malicious files to steal data and control devices. Read More...…

Jul 05, 2024

Tips for Identifying Genuine Bank Communications

In this blog, we will guide you on identifying genuine bank messages and tips to protect yourself from cybercrime scams.

Jul 01, 2024

Unlock Financial Freedom: The Perks of Zero Balance Accounts

A Zero Balance Account benefits students, young professionals, and anyone seeking streamlined banking. Here are its advantages and why it’s right for you.…

Jun 26, 2024

The Risks of Juice Jacking: Tips to Keep Your Data Safe

In this blog, we will explore juice jacking, a cybercrime where public USB charging ports steal sensitive information from your device. Read More....

Jun 21, 2024

Lost or Stolen Credit Card? Here’s Your Step-by-Step Guide

This blog covers the essential steps to take if your credit card goes missing, offering a simple and straightforward process. Read more...

Jun 10, 2024

How Cyber Insurance Can Save Yourself from Financial Loss

Learn how cyber insurance protects against cyber-attacks and how the RBL Bank GO Savings Account offers free coverage.

May 31, 2024

How do Credit Cards Work?

In this blog, we will explain what credit cards are, how they work, and provide tips for using them responsibly to make informed financial decisions.

May 27, 2024

10 Common Credit Score Myths You Should Know

In this blog, we'll debunk common credit score myths, providing clarity to help you make smarter financial decisions.

May 15, 2024

Parcel Scams: How to Spot and Avoid Them

This blog highlights parcel scams in online shopping, where scammers pose as delivery services to steal info or money. Stay alert.

May 06, 2024

Newly Married? Here are 5 Financial Tips to Plan your Future

In this blog, we'll explore key financial advice for newlyweds, covering joint financial planning, emergency funds, investment options, and beyond.

Apr 26, 2024

Step-by-Step Guide to Open RBL Bank’s GO Savings Account

Discover how RBL Bank’s GO Savings Account simplifies banking with digital ease, no balance requirement, and premium perks.

Apr 19, 2024

How to Spot and Avoid Dangerous Apps

Explore the dangers of apps from unauthorized sources, including malware, data breaches, and financial scams.

Apr 05, 2024

How to Save on Income Tax? A Step-By-Step Guide

In this blog, we'll explore Income Tax in India, unraveling its structure, discussing tax-saving strategies, and helping you navigate the system.

Mar 20, 2024

4 Ways to Save Tax with your Home Loan

Discover 4 essential ways to maximize tax savings and achieve your dream homeownership.

Mar 15, 2024

The Evolution of Women: From Penny Pinching to Power Planning

Celebrating women's financial empowerment, offering tailored banking solutions and resources for informed decision-making and independence.

Mar 07, 2024

Building the Foundation: The Power of Saving & Compounding

Saving is the process of putting money away for future use instead of spending it right away.

Mar 01, 2024

Financial Literacy Week 2024: Make a Right Start with Secure Online Ha..

Learn the best practices for online safety to help you navigate through the digital world with resilience and peace of mind.

Feb 29, 2024

How to Open a Digital Savings Account?

Opening a Digital Savings Account needs Aadhaar, PAN Card details and verification. Know these steps before opening a Digital Savings Account.

Feb 23, 2024

What are the types of Fixed Deposits?

Secure your future with Fixed Deposits (FDs) for guaranteed returns and flexible investment options. Learn more about different types of FDs.

Feb 09, 2024

How to Protect Passwords? Risks, Frauds, and Security Measures

Learn to protect your digital identity from hackers and scams with smart password choices and strong security measures.

Feb 07, 2024

Elevate Your Finances with RBL Bank’s GO Digital Savings!

RBL Bank's GO Digital Savings offers a zero-balance account with unlimited ATM withdrawals and a premium debit card.

Jan 25, 2024

How much money should you keep in your savings account?

A Savings Account offers more than saving; it’s a versatile tool with many benefits. This guide helps you navigate today’s financial landscape.

Jan 18, 2024

Ways to Protect Yourself Against Social Media Frauds

Beware of rising social media frauds! From phishing to identity theft, scammers exploit digital platforms. Learn to protect yourself from these scams.

Jan 03, 2024

What are the advantages of Digital FD?

Digital Fixed Deposits offer numerous advantages, transforming how you secure your financial future. Let's explore the key benefits of choosing digital FDs…

Dec 30, 2023

8 Things You Should Consider Before Applying for an Education Loan

Education loans are a vital financial tool, supporting students globally. Here are some key benefits of education loans.

Dec 22, 2023

What is Net Banking? A Complete Guide

Internet banking, also known as Net Banking, isn’t just a service, it’s a financial friend that speaks the lingo of modern India.

Dec 15, 2023

A Complete Guide to the Home Loan Process in India

In this blog, we will explore the essential steps, benefits, and requirements of the home loan process in India.

Dec 08, 2023

Zero Balance, Maximum Benefits: RBL Bank’s GO Account

If you're looking for a way to save without having to worry about maintaining minimum balance, a Zero Balance Account is the way to go! Read More....

Nov 20, 2023

How to Safeguard yourself from Voice Cloning Fraud

Voice cloning mimics another person's voice using text-to-speech software, deep learning, and large audio datasets. Read more...

Nov 13, 2023

How to make the best use of Credit Cards this festive season?

Let's look at how credit cards can transform your life this festive season, from reward points to bank partnerships.

Nov 02, 2023

Safeguarding Your Identity: A Roadmap to Theft Prevention

Identity theft is one such threat that involves stealing individual’s personal or financial data to use their identity for fraudulent activities. Read More…

Oct 06, 2023

How to get a Loan Against Property? Tips & Benefits

A Loan Against Property is a type of secured loan that lets you pledge your home or commercial real estate as collateral.

Sep 30, 2023

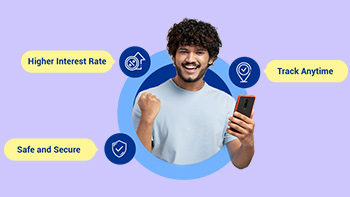

Open Digital Fixed Deposit at Attractive Interest Rates

Digital Fixed Deposits allow you to earn assured returns on savings online. Some banks let you open an FD without needing a savings account.

Sep 16, 2023

8 Common Banking Scams and How to Prevent Them

Read on to find out the different ways in which you could get caught in the web of cybercrime, in order to stay alert at all times.

Aug 01, 2023

Benefits of using Credit Cards for everyday purchases

In this blog, we’ll explore some tips and strategies for you to use your credit card wisely and make the most of its benefits.

Jul 24, 2023

Discover the Benefits of Yoga on International Yoga Day

Here’s why should you make Yoga a part of your daily routine. This Yoga day revisit and strengthen your commitment to Yoga.

Jun 20, 2023

A Complete Guide and Checklist to Efficient Tax Filing

Filing your taxes on time is also important because it is a legal requirement. Here’s a checklist to follow.

Jun 09, 2023

Protect yourself from UPI Frauds

UPI frauds are becoming more sophisticated, so users must stay vigilant and take precautions to protect themselves.

Jun 07, 2023

5 ways to teach children financial responsibility

In this blog, we explore how to teach kids financial responsibility and help them develop smart money habits from an early age.

Apr 17, 2023

Everything to know about PAN Card fraud

This blog post provides valuable insights into PAN Card fraud, including options to check PAN Card fraud and ways to prevent falling victim to them.

Apr 03, 2023

Emergency Fund Guide: How to Prepare for Unexpected Expenses

Emergency fund is the ultimate solution to prevent debts from loans and overdrafts. Here are a few suggestions that can get you started.

Mar 09, 2023

NRE vs NRO and FCNR Accounts: Know the Complete Differences

If you're an NRI looking to open a bank account in India, this article covers the three main types: NRE, NRO, and FCNR.

Feb 23, 2023

Everything to know about Online Frauds

Stay informed and protected with the latest insights on online frauds, from prevention to recovery tips.

Jan 31, 2023

A Complete Guide to ATMs: Benefits, Purpose, and Tips

ATM has truly transformed the way we manage funds online. Learn more about its features and safety tips.

Jan 13, 2023

What is KYC? and How important it is in Fixed Deposit

KYC (Know Your Customer) is an RBI-regulated identity verification process. Learn about its full form, types, and importance in Fixed Deposits.

Dec 30, 2022

Fixed Deposit Premature Withdrawal and the Impact on Interest Calculat..

The FD premature withdrawal penalty calculator shows your earnings on existing Fixed Deposits. Learn about the implications of early withdrawal.

Dec 29, 2022

Ways to get the Best FD Rates in India

Discover how to secure the best bank FD rates for maximum short-term returns. Read our blog for tips!

Dec 21, 2022

Best Short-Term Investment Plans with High Returns in India for 2023 ..

Short-term investment plans can enhance your savings with higher returns. Let’s explore the top six options available.

Dec 20, 2022

How to Choose the Right Fixed Deposits (FD) for Investment?

Learn more about the higher rates on different fixed deposit types as per your financial planning. Compare & choose which FD is best for your investment…

Dec 13, 2022

Certificate of Deposit Vs Fixed Deposit

Discover the differences between Certificates of Deposit (CD) and Fixed Deposits (FD), including their meanings, benefits, and rates.

Dec 08, 2022

Understand 10 Money Saving Tips to Achieve your Goals

Here are 10 crucial money-saving tips to secure your financial future and better plan your budget.

Dec 08, 2022

Difference between Savings Account and Fixed Deposit Account

Explore the differences between a savings account and a fixed deposit (FD), including their meaning, benefits, and interest rates.

Dec 07, 2022

Difference Between Cumulative and Non-Cumulative FD

Learn more about the difference between Cumulative Fixed Deposits (FD) vs Non-Cumulative Fixed Deposits (FD).

Dec 02, 2022

Bank Fixed Deposits and Corporate Fixed Deposits: Major Advantages and..

Discover the differences between Bank and Corporate Fixed Deposits to determine the best option for your needs.

Nov 29, 2022

What is the difference between Term Deposit and Fixed Deposit?

Explore the differences between term and fixed deposits, including flexibility, interest rates, tenure, and profit potential in risk-free investments.

Nov 29, 2022

What is a Fixed Deposit? Know the meaning & features of FD

A fixed deposit lets you invest for a set term and earn fixed returns. Learn about its definition, characteristics, and functionality.

Nov 22, 2022

What are the types of Fixed Deposits?

Discover different types of FDs for various investment purposes to secure your financial future. Explore risk-free options.

Nov 22, 2022

How does Fixed Deposit Account Work?

A Fixed Deposit lets you invest for a fixed term and earn maximum returns at a fixed interest rate. Learn how fixed deposits work in India.

Nov 18, 2022

How does a bank calculate interest on your FD?

To calculate interest on fixed deposits, use the formula (PxRxT/100) or [P * {(1+R/100) ^ T}] - P. Check out RBL Bank's FD calculator for more.

Nov 18, 2022

Short-Term or Long-Term Fixed Deposit: Which One To Choose?

Explore the differences between Short Term and Long Term FDs, including definitions, benefits, eligibility, and interest rates.

Nov 07, 2022

Fixed Deposits vs Equity Investments – A Compressive Guide

Understand the differences between Fixed Deposits and Equity Investments, covering definitions, risks, returns, and benefits.

Nov 01, 2022

Fixed Deposits vs Liquid Funds: A Detailed Guide

Compare liquid funds and fixed deposits to make informed decisions, including definitions, benefits, eligibility, and interest rates.

Nov 01, 2022

7 Types of Bank Frauds Everyone Should Know

From mobile phones to the internet, know the different types of scams that the fraudsters run to steal your identity and your money!

Oct 28, 2022

Fixed Deposit vs Mutual Funds: Which is Best to Invest?

Explore the differences between Fixed Deposits and Mutual Funds, including definitions, benefits, comparisons, eligibility, and interest rates.

Oct 27, 2022

Fixed Deposit Vs Public Provident Fund: Which is Good?

Learn the differences between Fixed Deposits (FD) and Public Provident Fund (PPF), including their definitions, benefits, eligibility, and interest rates.…

Oct 27, 2022

What is the difference between a Fixed Deposit and a Recurring Deposit..

Compare fixed deposits and recurring deposits, covering definitions, benefits, eligibility, and interest rates.

Oct 20, 2022

Fixed Deposits: Ideal Investment Options for Beginners

New to investing? Fixed Deposits offer high returns, low risk, and easy liquidity - an ideal choice for beginners.

Oct 18, 2022

Digital Banking Frauds & How Can We Safeguard Ourselves?

In this blog, we will explore the rise of digital banking fraud and share effective strategies to safeguard your finances.

Sep 27, 2022

Get To Know Exactly What Convenience Banking Is All About!

In this blog, we will explore how convenience banking simplifies your financial activities with easy and accessible services.

Sep 07, 2022

What is Tokenisation and how important is it for you to use?

Tokenisation will offer an additional layer of security to users' sensitive data, preventing online and digital data breaches. Read More...

Aug 26, 2022

How Digital Savings Account differs from a Savings Account

Digital Savings Accounts are popular for quick, easy access and differ from traditional Savings Accounts in five key ways.

Aug 02, 2022

6 reasons to buy health insurance at a young age

From lesser premiums to tax benefits, here are six reasons why insurance is considered the first step in investment planning.

Jul 28, 2022

Vigilance - Key to avoid being a victim of online frauds

With online banking frauds on the rise, some simple precautions can help you keep your account and money secure.

Jul 05, 2022

4 Reasons why you need the RBL Bank Cookies Credit Card

The RBL Bank Cookies Credit Card covers all expenses, from groceries and fuel to luxury purchases and online shopping.

Jun 23, 2022

5 Methods to Report a Lost or Stolen Debit Card

How to report a stolen or a lost debit card to the bank directly from your mobile. Read Here.

Jun 16, 2022

The definitive guide on salary and savings accounts

Understand the differences and similarities between a savings account and a salary account.

Jun 06, 2022

To #RahoCyberSafe, read some recommendations from our blog

This blog highlights some common scam methodologies and recommends a few best practices to stay vigilant in such scenarios.

May 30, 2022

How to achieve short term goals with Recurring Deposit

Recurring Deposit is one of the best products to help create a habit of saving for the future.

Apr 27, 2022

The many faces of Digital Banking

Learn how 'Digital Banking' is changing the lives of internet users from different walks of life.

Apr 05, 2022

Learn how to secure yourself from QR code scams

Let us take a look at the most common types of QR code scams and how to protect one’s savings & bank balances from such scams.

Apr 04, 2022

Decoding the Old and New tax regime

This blog will help you identify the right tax regime with a detailed list of exemptions, deductions, and tax rates.

Mar 09, 2022

How to select the perfect Savings Account #SavingsHaiAsaan

The blog highlights how to choose the right savings account, showcasing personal stories and emphasizing RBL Bank's features and benefits.

Feb 28, 2022

A gentle reminder on how to use the internet safely

From cyberbullying to safe mobile banking, here is a definitive guide of handling the internet safely.

Feb 17, 2022

Walk into the new year with a financial plan in place

As we walk into another, hopefully better year, here are 5 golden tips about financial planning to help you manage your money better.

Dec 22, 2021

Reasons why you should switch to Mobile Banking

RBL Bank's MoBank app ensures that all your banking needs are available right at your fingertips.

Nov 11, 2021

Digital Savings Account: Innovation in Convenience Banking

Looking for a reliable banking partner that lets you transact with convenience on the go? Here's what you get with RBL Bank's Digital Savings Account.

Oct 20, 2021

The New Normal of Convenience Banking

The evolution of the traditional savings account, and 5 ways to make your digital savings account work for you!

Oct 07, 2021

Tips to keep your OTP safe from online fraud

Online frauds have surged with the rise in digital transactions during the COVID-19 lockdown. It’s crucial to keep your OTP safe. Here are some tips.

Oct 04, 2021

Steps to take if you are victim to a credit card fraud

Let us take a look at the different kinds of credit card scams and Immediate steps to take when you have been scammed.

Sep 07, 2021

Tips to protect seniors from online frauds

Seniors citizens are often targeted by online scammers. Here are a few tips that will help them protect themselves from online frauds.

Aug 24, 2021

The millennial guide to studying abroad

Here are a few pointers that will help international students to transform outbound journey into a seamless experience.

Jul 26, 2021

Thank you to every Dad for being the best financial advisor

On the occasion of Father’s Day, let’s revisit some of the best financial advice given by all the Dads ever since our childhood days.

Jun 18, 2021

Go Green with Digital Banking this World Environment Day

Here’s a quick guide on how you can help to keep the world greener while you embrace the benefits of Digital Banking.

Jun 04, 2021

How Smishing works & ways to avoid it

Do you know what Smishing is and how it works? Read how to avoid getting lured by Smishing attacks.

May 17, 2021

Best Financial Gifts For Your Mother

This article seeks to shed light on viable financial gifts that can be gifted to all mothers this Mother’s Day.

May 07, 2021

How to choose the ideal RBL Bank Debit Card for yourself

Want to avail the ideal debit card that fits your requirements? Here’s everything you wanted to know.

Jan 26, 2021

Experience the new way of contactless banking

Get ready for uninterrupted contactless banking journey with seamless services, smart and secure features and a lot more.

Oct 13, 2020

All about CIBIL Score and how is it calculated

If you are looking for credit, you must have heard about the CIBIL Score from a lot of people around you. Let’s find out what it is, how it works, and why…

Aug 06, 2020

What is the difference between CIBIL Score and CIBIL Report?

Are you new to the world of credit and confused with all the terms coming your way? Want to know the difference between CIBIL Score and CIBIL Report? Here…

Jul 30, 2020

What does a 'Settled' status in your CIBIL report mean?

Most people would have a hard time understanding whether a 'settled' status on your CIBIL report is a positive or negative. Read on to understand this…

Jul 10, 2020

Five ways to get started on your savings journey

As you start earning, future goals may seem distant, but saving early is a smart habit. Here are 5 ways to kickstart your savings journey.

Dec 30, 2019

Things to Note Before Applying for a Credit Card

If you’re decided on owning a credit card and are applying for one, here are some essential points to consider.

Dec 30, 2019

Basic banking processes you can teach your kids

For children to imbibe financial discipline, essential for addressing life goals, it’s important for them to be familiar with the basic banking exercises.…

Dec 28, 2019

Understanding your credit card statement

The credit card statement highlights every detail. Most of the times, the only important aspect considered is the amount due. Nonetheless, there are various…

Dec 19, 2019

5 hot new cuisines you should consider exploring

It is often said that the best way to experience a culture and a country is by experiencing its food. Here are some hot new cuisines you should consider…

Dec 17, 2019

How to reset your PIN online

A PIN is the easiest way to keep your account safe. It’s good practice to keep changing it frequently. Here’s how to reset it.

Dec 11, 2019

How to redeem Credit Card reward points

Credit Card reward points can be redeemed for different products and services. Here is how to go about it.

Dec 11, 2019

5 advantages of using your Credit Card internationally

Credit cards are useful for international travel, enabling cash-free payments. Here’s a look at additional benefits.

Dec 11, 2019

How to build your credit score while swiping your Credit Card

Did you know a good credit score helps you access loans and credit products? Let’s discuss what a credit score is and how to improve yours.

Dec 11, 2019

Have a Credit Card? Here’s why you need another

In this blog, we will explore how multiple credit cards can improve rewards, credit scores, and management.

Dec 11, 2019

Things to Know Before Swiping Your Credit Card at an ATM

Here are some important things to know before you use your Credit Card at an ATM.

Dec 11, 2019

Eating out & Credit Card

RBL Bank’s range of Credit Cards will ensure that you embrace the foodie in you. Let’s look at some of the food options available.

Dec 11, 2019

Essential tips for Safe Banking

In the digital age when most banking activities are done online, it’s essential to be even more cautious. Here are some key tips for safe banking.

Nov 26, 2019

Best ways to carry foreign currency while travelling abroad

We have outlined the best ways available to you to carry foreign currency for a travel abroad, whether for business or a vacation.

Nov 26, 2019

Fostering women entrepreneurship in rural India through financial incl..

The empowerment of women is essential for achieving the objective of inclusive, equitable and sustainable development and economic growth in any nation.

Nov 26, 2019

What is a Credit Score & why is it important?

A credit score is a three-digit number assigned by a Credit Information Companies (CIC) to a borrower based on his or her track record WRT earlier and…

Nov 26, 2019

How Mobile Banking is transforming traditional banking

Mobile banking's rise is driven by Digital India policies, better connectivity, and its inherent benefits.

Nov 26, 2019

Benefits of owning multiple credit cards

Multiple cards give you access to a large amount of credit. It helps you make the most of the interest-free period. When used wisely, having more than one…

Nov 26, 2019